Market Commentary - May 2026

Equity markets staged a remarkable rally in April, pushing year-to-date returns into positive territory. The rally was driven by easing geopolitical concerns in the Middle East, resilient first-quarter earnings, and renewed enthusiasm around artificial intelligence and growth-oriented sectors. At the same time, the macro backdrop remained complex, with higher energy prices and firm inflation tempering expectations for near-term Federal Reserve rate cuts. What follows highlights how markets reconciled these crosscurrents, ultimately rewarding underlying earnings strength despite ongoing uncertainty.

| Index | April 2026 (%) | YTD (%) | 1-Year (%) | 3-Year Annualized (%) |

| S&P 500 Index | 10.5 | 5.7 | 31.0 | 21.6 |

| Dow Jones Industrial Average | 7.2 | 3.8 | 24.2 | 15.4 |

| NASDAQ Composite Index | 15.3 | 7.3 | 43.6 | 27.6 |

| Russell 2000 Index | 12.3 | 13.3 | 44.6 | 18.2 |

| MSCI All Country World Index (ex U.S.) | 9.7 | 9.1 | 33.0 | 18.0 |

| MSCI Emerging Markets Index | 14.7 | 14.6 | 47.5 | 21.2 |

| U.S. Aggregate Bond Index | 0.1 | 0.1 | 4.1 | 3.5 |

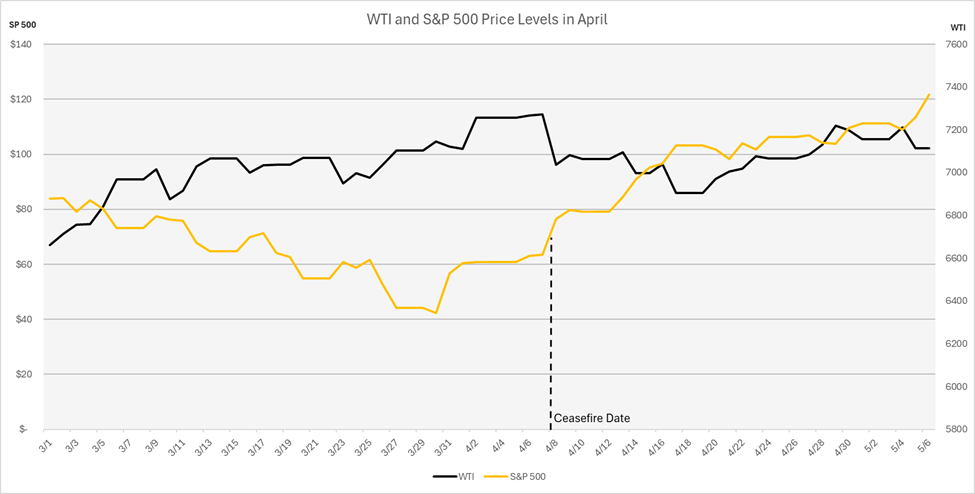

April marked a sharp reversal from the risk-off tone that defined the first quarter, with global equities delivering one of their strongest monthly performances in years. The S&P 500 Index advanced approximately 10.5%, its best month since late 2020, while the NASDAQ Composite Index (NASDAQ) surged more than 15% and the Dow Jones gained over 7%, with several indices reaching new all-time highs. In many respects, markets climbed a familiar “wall of worry,” quickly recovering March’s losses and signaling a renewed willingness among investors to look through near-term volatility toward longer-term earnings growth.

From Escalation Risk to Stabilization Risk

April brought a meaningful shift in tone across the geopolitical landscape, one that quickly reverberated through global financial markets. On April 8, the United States and Iran agreed to a two-week ceasefire brokered by Pakistan, pausing a conflict that had unsettled investors and disrupted global energy markets since late February. Markets responded swiftly. The Dow Jones Industrial Average surged more than 1,000 points in early trading, while the S&P 500 Index and NASDAQ followed with broad-based gains, supported by strength across Asian and European markets.

Energy markets moved just as decisively. Oil prices fell sharply on expectations that disruptions through the Strait of Hormuz, which carries roughly 20% of global oil supply, could begin to ease after weeks of constrained flows. Importantly, while the conflict itself remained unresolved, the perceived trajectory shifted. Investors began to price in a lower probability of worst-case outcomes, particularly around prolonged supply disruptions and broader regional escalation.

Some market strategists, however, cautioned that the rally may have outpaced the underlying improvement in fundamentals. Much of the initial surge appeared to reflect the unwinding of hedges and short positions rather than a durable change in the geopolitical backdrop. Unlike prior market disruptions driven by policy or trade negotiations, the dynamics in the Middle East remain inherently less predictable and less controllable, raising the risk that markets may be over-discounting near-term stability.

This stands in contrast to the environment we described last month. In March, geopolitical risk escalated rapidly as conflict between the United States, Israel, and Iran expanded beyond bilateral lines, forcing markets to reassess inflation risk, monetary policy expectations, and the durability of elevated oil prices. That escalation defined the quarter’s risk-off tone. April, by comparison, marked not a resolution, but a recalibration, as markets shifted from pricing escalation toward cautiously pricing stabilization.

Earnings Brought the Receipts

Once the headlines stopped getting worse, the market did what it usually does: it went back to earnings. Corporate earnings were the second major driver behind April’s outsized gains. With geopolitical risk no longer worsening by the day, investors pivoted back to fundamentals and earnings season delivered a surprisingly strong set of results. FactSet’s blended S&P 500 Index earnings growth rate for the first quarter rose to 27.1%, supported by an unusually high share of companies beating expectations. However, the headline figure deserves a footnote: Alphabet, Amazon, and Meta accounted for the majority of the period’s earnings upside, and their GAAP results were boosted by items that are difficult to repeat, including investment-related gains and a sizable tax benefit. In other words, earnings were strong, but not evenly sourced, and part of the strength reflected accounting tailwinds tied to the AI investment cycle rather than purely operating momentum.

Importantly, even after adjusting for concentration and one-time items, the broader earnings backdrop remains firm. The 27.1% growth rate would mark the strongest quarterly increase in S&P 500 earnings since late 2021, and the strength has not been isolated to a handful of names. Seven of eleven sectors are currently reporting double-digit earnings growth, led by Communication Services, Information Technology, and Consumer Discretionary, while nine sectors in total are delivering year-over-year gains. This breadth reinforces the idea that underlying corporate profitability remains intact, even in the face of elevated energy prices and geopolitical uncertainty. Put differently, while the headlines were helped by a few outsized contributors, the foundation beneath that growth appears far more durable and broadly supported than the top-line figure alone might suggest.

Economic Growth, Jobs, and Prices: A Mixed but Durable Backdrop

If earnings provided the fuel for April’s rally, the economic data offered reassurance that the engine is still running. The broader economic backdrop helped reinforce that narrative, with incoming data pointing to resilience rather than reacceleration. First-quarter GDP growth came in at approximately 2.0% annualized, an improvement from the prior quarter but modestly below expectations, reflecting an economy that continues to expand, albeit at a more measured pace. Labor market conditions remained firm, with payroll growth exceeding expectations and the unemployment rate holding near 4.3%, suggesting that underlying demand has yet to meaningfully deteriorate despite higher interest rates and elevated energy costs. Inflation, however, remains a complicating factor. Headline CPI accelerated to roughly 3.3% year-over-year, driven in large part by higher energy prices tied to geopolitical disruptions, reinforcing the view that the Federal Reserve will need to remain patient in considering any policy easing. Taken together, the data depict an economy that is neither overheating nor rolling over but instead continuing to grow through a more challenging macro environment—a combination that has historically been supportive of corporate earnings, even if it leaves less room for policy flexibility.

A closer look at the GDP report highlights just how concentrated that growth was beneath the surface. Nonresidential business investment alone contributed roughly 1.4 to 1.5 percentage points to the 2.0% annualized growth rate, making it the single largest driver of the quarter. By comparison, consumer spending added just over 1 percentage point, reflecting a noticeable deceleration in household activity. The strength in investment was driven largely by equipment and intellectual property spending, categories that increasingly reflect the ongoing buildout of artificial intelligence infrastructure, including data centers, software, and computing equipment. In that sense, the composition of the GDP report tells a more nuanced story: headline growth remains solid, but it is being supported disproportionately by a capital spending cycle tied to AI, rather than broad-based demand across the traditional pillars of the economy.

Rates on Hold, Pressure Building

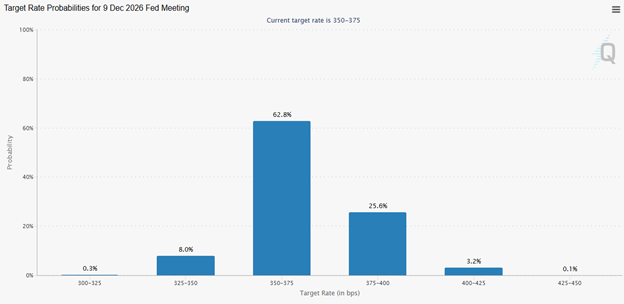

While economic data pointed to resilience, the Federal Reserve reminded markets that patience is still firmly in place. At its April 29 meeting, the Federal Reserve held the federal funds rate steady at a range of 3.50% to 3.75% for the third consecutive meeting, citing an economy that continues to expand at a solid pace alongside persistently elevated inflation. The decision was far from unanimous, however, with four dissenting votes marking the highest level of disagreement among policymakers in decades and underscoring just how uncertain the policy path has become. Against that backdrop, the focus quickly shifted from rates to leadership. The Senate Banking Committee advanced Kevin Warsh’s nomination as the next Federal Reserve Chair, setting up a full Senate confirmation vote that is widely expected ahead of Jerome Powell’s term ending May 15. In a notable departure from precedent, Powell indicated he will remain on the Board of Governors beyond his chairmanship, emphasizing that the Federal Reserve’s independence must be preserved amid ongoing political and legal challenges. Taken together, the meeting reinforced a familiar message on policy, data dependent and patient, but introduced a new layer of uncertainty around governance, as the central bank navigates a leadership transition at a time when inflation remains above target and consensus within the Committee is increasingly difficult to achieve.

Market pricing, as illustrated in the accompanying chart, reflects that same cautious tone, with futures markets currently assigning a higher probability to rates moving modestly higher rather than lower by year-end, suggesting investors increasingly believe the next move could be a hike if inflation and growth data remain firm.

The Case for Optimism, with Discipline

Stepping back, the combination of earnings, economic data, and policy signals paints a more balanced picture than the headlines alone might suggest. While recent data have not been without their inconsistencies, the underlying trend remains encouraging. Earnings growth is not only strong, but increasingly broad-based across sectors, reinforcing the idea that corporate profitability is not solely reliant on a narrow set of drivers. At the same time, economic data continue to point to a stable, if unspectacular, expansion, supported by a resilient labor market and ongoing business investment. Even the geopolitical backdrop, while still fluid, appears to have moved past its most disruptive phase, with markets showing signs of adjusting to a higher but more stable energy regime. Taken together, these factors suggest a foundation that is more durable than it may first appear. While risks remain, particularly around inflation and policy uncertainty, the combination of improving earnings breadth, steady economic activity, and a less acute external shock environment provides a constructive backdrop that supports a cautiously optimistic outlook for the remainder of the year.

Looking Ahead

As the first four months of the year have reinforced, markets can be remarkably inefficient in the short term. Periods of uncertainty, whether driven by policy shifts, geopolitical tension, or uneven economic data, often take time to fully play out in asset prices. Yet history continues to remind us that over the longer term, market outcomes tend to move in cadence with underlying earnings growth. With corporate profits expanding, participation broadening across sectors, and the economic backdrop remaining stable, the foundation for equities appears intact. While near-term volatility should be expected as markets digest shifting policy expectations and global developments, the longer-term trajectory remains tied to the ability of companies to grow earnings, a dynamic that, at present, continues to lean constructive.

Thank you for your continued confidence in our team, and please reach out with any questions you may have. It is our pleasure to share life’s journey with you.

Market Commentary Disclosures

*Magnificent Seven: The term "Magnificent Seven" was coined by others and should not be construed as an endorsement or indicator of any stock or company's quality.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from Towne Trust to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions as of the date given and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Neither past performance or yields are reliable indicators of current and future results.

Stock investments involve risk, including loss of principal. High-quality stocks may be appropriate for some investment strategies. Ensure that your investment objectives, time horizon and risk tolerance are aligned with investing in stocks, as they can lose value. Although we define “high quality” stocks as having high and stable profitability (return on equity, earnings variability) the term “high quality” is not a recommendation for any specific investment as stocks may not be appropriate for some investment strategies.

There are risks associated with fixed-income investments, including credit risk, interest rate risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced for longer term securities. A rise in interest rates may result in a price decline of fixed-income instruments held by the fund, negatively impacting its performance and NAV. Falling rates may result in the fund investing in lower yielding debt instruments, lowering the fund’s income and yield. These risks may be heightened for longer maturity and duration securities.

Towne Trust, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein.

Not FDIC Insured • May Lose Value • Not Bank Guaranteed • Not a Deposit

Index Definitions

Dow Jones Industrial Average: The Dow Jones Industrial Average is a price-weighted average of the 30 blue chip stocks that are generally the leaders in their industry. It has been widely followed indicator of the stock market since October 1, 1928.

NASDAQ Composite Index: The NASDAQ Composite Index is a broad-based capitalization-weighted index of stocks in all three NASDAQ tiers: Global Select, Global Market and Capital Market. The index was developed with a base level of 100 as of February 5, 1971.

Russell 2000 Index: The Russell 100 Index is comprised of the smallest 2,000 companies in the Russell 1000 Index, representing approximately 8% of the Russell 3000 total market capitalization. The real-time value is calculated with a base value of 135.00 as of December 31, 1986. The end-of-day value is calculated with a base value of 100.00 as of December 19,1978.

S&P 500 Index: The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products. The index includes 500 leading companies and captures approximately 80% coverage of the available market capitalization.

MSCI Emerging Markets Index: The MSCI EM (Emerging Markets) Index is a free-float weighted equity index that captures large and mid-cap representation across Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in the each country.

U.S. Aggregate: The Bloomberg USAgg Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (Agency fixed-rate pass-through), ABS and CMBS (agency and non-agency). (Future Ticker: I00001US)

MSCI ACWI Excluding United States Index: The MSCI AC World ex USA Index is a free-float weighted equity index. It was developed with a base value of 100 as of December 31, 1987.

About the Author