Market Commentary - March 2026

February reflected a market pulled in several directions at once. Returns were uneven as investors balanced geopolitical risk, renewed inflation concerns, and trade policy uncertainty against a still constructive earnings backdrop. Worries about the durability of SaaS business models in an AI driven world continued to pressure software stocks, while capital rotated toward asset heavy HALO companies with lower obsolescence risk. Strong corporate profits helped offset those concerns, though a hotter inflation print and tariff headlines late in the month reinforced the sense that progress remains uneven rather than smooth.

| Index | February 2026 (%) | YTD (%) | 1-Year (%) | 3-Year Annualized (%) |

| S&P 500 Index | (0.8) | 0.7 | 17.0 | 21.8 |

| Dow Jones Industrial Average | 0.3 | 2.1 | 13.6 | 16.6 |

| NASDAQ Composite Index | (3.3) | (2.4) | 21.1 | 26.5 |

| Russell 2000 Index | 0.8 | 6.2 | 23.4 | 13.1 |

| MSCI All Country World Index (ex U.S.) | 5.0 | 11.4 | 40.6 | 20.6 |

| MSCI Emerging Markets Index | 5.5 | 14.9 | 50.8 | 22.1 |

| U.S. Aggregate Bond Index | 1.6 | 1.8 | 6.3 | 5.1 |

February total returns were mixed across asset classes, consistent with the month’s historical tendency toward higher volatility. U.S. equities generally declined, led by weakness in Large Cap Growth and technology-dominated indices as investors reassessed elevated valuations and accelerating artificial intelligence (AI) fears, while Small Cap stocks held up better amid a rotation toward more domestically focused and cyclical companies. The Energy and Utilities sectors posted double-digit returns, while the Financials, Technology, and Consumer Discretionary sectors each declined by four percent. Yields across the intermediate portion of the Treasury curve (two to ten years) declined to trailing twelve-month lows, providing a meaningful tailwind to returns in the U.S. Aggregate Bond Index.

Worry is a Feature of Markets, not a Forecast

Late in February, geopolitical risk escalated sharply as the United States and Israel launched coordinated strikes on Iran that, according to Iranian state media, killed Ayatollah Ali Khamenei and raised immediate questions about political succession in Tehran. Iran’s response was swift and regional, with missile and drone attacks directed not only at Israel but also at U.S. military assets and neighboring Gulf states that host American forces, reinforcing long standing warnings that any direct confrontation would quickly spill beyond bilateral lines. The conflict also introduced tangible economic risks, particularly to energy markets, as shipping through the Strait of Hormuz faced renewed disruption concerns and oil prices began to reflect a higher geopolitical risk premium. As with many geopolitical crises, events are evolving so rapidly that by the time this commentary reaches readers, both the facts on the ground and the market’s interpretation of them will almost certainly look materially different.

The SaaS Apocalypse

While geopolitics dominated the headlines, a quieter but potentially more consequential shift continued to unfold within equity markets, particularly across software and cloud companies, where rapid advances in artificial intelligence are raising fundamental questions about whether large portions of the traditional software as a service (“SaaS”) stack remain necessary at all. For much of the past decade, SaaS companies occupied a privileged position in the economy, acting as essential intermediaries between people, data, and business processes. That role is now being challenged in a more fundamental way than investors initially expected. Advances in artificial intelligence are increasingly allowing users to bypass traditional software layers altogether, shifting tasks from navigating applications to simply expressing intent. In this emerging model, value accrues less to the software interface and more to the intelligence embedded beneath it, raising a difficult question for some SaaS businesses: if AI can understand, execute, and adapt directly, what purpose does the application itself still serve?

At the same time, it is probably too simplistic to conclude that software is headed for extinction. In several parts of the enterprise, SaaS platforms still do important work that AI alone cannot easily replace, such as enforcing permissions, maintaining clean and auditable data, and coordinating activity across large organizations. That reality helps explain why companies like Salesforce and ServiceNow are not trying to step out of the way of AI, but instead are pulling it deeper into their platforms so that agents operate inside established systems of record rather than around them. A similar logic shows up at Atlassian, where recent product updates are designed to let humans and AI agents work side by side within familiar workflows, instead of forcing organizations to abandon structure altogether. Even Microsoft, whose Copilot strategy arguably accelerates the pressure on traditional applications, has been clear that identity, governance, and enterprise control remain central as interfaces evolve. The more likely outcome, then, is not that SaaS disappears, but that its role becomes narrower and more demanding, with real value accruing only to platforms that can anchor AI safely, reliably, and at scale.

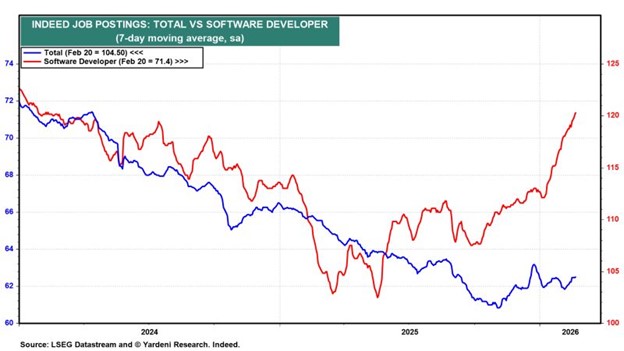

As Ed Yardeni, president of Yardeni Research, points out, concerns that AI will hollow out software employment have grown louder, yet Indeed data show software developer job postings still running 11% above year ago levels.

The HALO Effect

In the wake of the SaaS apocalypse narrative, many investors have gravitated toward what we call HALO stocks, meaning heavy assets and low obsolescence. These are businesses built around physical infrastructure or regulated systems that are hard to replicate and unlikely to be rendered irrelevant by a better algorithm. Think of pipeline operators like Kinder Morgan or Enbridge, railroads such as Union Pacific and CSX, utilities like NextEra Energy or Duke Energy, industrial manufacturers such as Caterpillar, and defense contractors including Lockheed Martin and Northrop Grumman. Unlike software companies, whose products can be bypassed or rebuilt as AI advances, HALO businesses tend to sit closer to physical reality, where permits, scale, engineering expertise, and decades long asset lives still matter. In a world where software feels increasingly optional, that kind of durability has become especially attractive.

But this rotation is not without its own risks, and some of them are old fashioned ones investors may be forgetting. A multitude of HALO stocks are cyclical, tied to economic growth, commodity prices, or government spending, and they often require substantial ongoing capital investment just to maintain their asset base. Free cash flow can look stable until a downturn exposes operating leverage or forces higher maintenance spending. At the same time, the rush toward perceived safety has pushed valuations for parts of the infrastructure, industrial, and defense complex above historical averages, quietly reducing future returns. In other words, HALO stocks may be harder to disrupt than SaaS or AI exposed names, but they are still subject to cycles, capital discipline, and valuation risk. They trade one set of uncertainties for another, which is precisely why selectivity matters as much here as it does anywhere else.

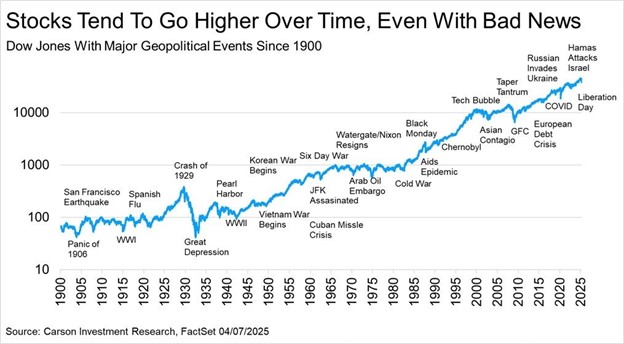

Stepping back, this chart is a useful reminder of how markets have behaved through history. Wars, pandemics, political crises, recessions, and technological revolutions have been constant features of the investment landscape, yet stocks have continued to compound higher over time. From the Spanish Flu and World War II to the internet boom and today’s AI revolution, the common thread has not been the absence of bad news, but the market’s ability to absorb it and move on. The lesson is not that risks do not matter, but that consistently trying to sidestep them has historically been far more damaging than staying invested. For long‑term investors, discipline and time in the market have remained the most reliable engines of wealth creation, even when the headlines felt overwhelming.

Earnings Still Doing the Heavy Lifting

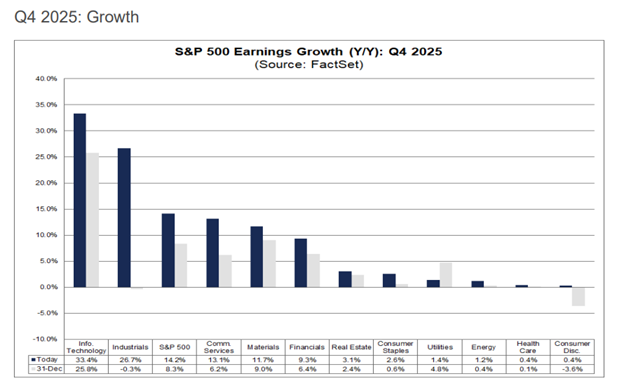

If markets ultimately move higher over time despite a steady stream of bad news, it is because earnings tend to do the same. And on that front, the latest reporting season has been quietly constructive. With nearly all S&P 500 companies now reported for the fourth quarter, earnings growth is tracking around the mid‑teens year over year, marking another consecutive quarter of double‑digit growth. Revenue growth has also remained solid, and profit margins are sitting near cycle highs, suggesting that corporate America has been better able to absorb higher costs and uncertainty than many feared.

That strength, however, is not evenly distributed, which helps explain some of the market’s crosscurrents. The largest technology and communication services companies continue to punch above their weight, while earnings growth for the rest of the index, though positive, is more modest.

At the same time, analysts have trimmed near‑term expectations for the first quarter, even as they have raised estimates for the back half of the year. In other words, the earnings picture looks less like a collapse and more like a pause, with valuations now doing more of the heavy lifting. As we move deeper into 2026, the market’s ability to push higher will increasingly depend not on headlines or narratives, but on whether earnings growth broadens beyond its current leaders and justifies the optimism already embedded in prices.

Inflation, Tariffs, and the Fed’s Dilemma

That focus on earnings briefly gave way at the end of February when inflation reentered the conversation. On February 27, 2026, the January core Producer Price Index surprised meaningfully to the upside, rising 0.8% month over month, well above expectations. The report pushed the year‑over‑year core PPI to 3.6% and revived concerns that price pressures, particularly in services, remain sticky. Markets reacted quickly, with equity futures moving lower following the release as investors reassessed the timing of potential Federal Reserve rate cuts and the risk that easing financial conditions had once again gotten ahead of inflation data.

Just a week earlier, policy uncertainty had come from a quite different direction. On February 20, 2026, the U.S. Supreme Court struck down the administration’s use of emergency powers to impose broad tariffs, a ruling that initially triggered a relief rally in tariff‑sensitive stocks and lifted broader equity indexes. That optimism proved short‑lived, however, as the White House quickly signaled alternative tariff measures, reintroducing uncertainty around trade, pricing, and supply chains. The result has been a familiar pattern for markets: sharp reactions to macro and policy headlines, followed by a return to the same underlying question of whether earnings growth can ultimately offset higher costs and policy noise.

Looking Ahead

As we move into March, seasonality begins to tilt more supportive, with markets historically finding firmer footing after the volatility that often characterizes the early part of the year. Attention will quickly turn to the Federal Reserve’s upcoming meeting, where policymakers are widely expected to hold rates steady, reinforcing the message that patience, rather than urgency, still defines the policy outlook. Alongside the Fed, investors will be watching a busy slate of economic data, including employment, CPI, and retail sales, for confirmation on whether inflation pressures are easing gradually or simply pausing. Layered on top of the macro calendar are ongoing geopolitical risks, from the Middle East to trade policy uncertainty, which remain capable of driving short‑term market swings.

Taken together, the near‑term environment still argues for realism rather than complacency, but also for perspective, as markets have repeatedly shown an ability to look through uncertainty when fundamentals remain intact.

Thank you for your continued confidence in our team, and please reach out with any questions you may have. It is our pleasure to share life’s journey with you.

Market Commentary Disclosures

*Magnificent Seven: The term "Magnificent Seven" was coined by others and should not be construed as an endorsement or indicator of any stock or company's quality.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from Towne Trust to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions as of the date given and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Neither past performance or yields are reliable indicators of current and future results.

Stock investments involve risk, including loss of principal. High-quality stocks may be appropriate for some investment strategies. Ensure that your investment objectives, time horizon and risk tolerance are aligned with investing in stocks, as they can lose value. Although we define “high quality” stocks as having high and stable profitability (return on equity, earnings variability) the term “high quality” is not a recommendation for any specific investment as stocks may not be appropriate for some investment strategies.

There are risks associated with fixed-income investments, including credit risk, interest rate risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced for longer term securities. A rise in interest rates may result in a price decline of fixed-income instruments held by the fund, negatively impacting its performance and NAV. Falling rates may result in the fund investing in lower yielding debt instruments, lowering the fund’s income and yield. These risks may be heightened for longer maturity and duration securities.

Towne Trust, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein.

Not FDIC Insured • May Lose Value • Not Bank Guaranteed • Not a Deposit

Index Definitions

Dow Jones Industrial Average: The Dow Jones Industrial Average is a price-weighted average fo the 30 blue chip stocks that are generally the leaders in their industry. It has been widely followed indicator of the stock market since October 1, 1928.

NASDAQ Composite Index: The NASDAQ Composite Index is a broad-based capitalization-weighted index of stocks in all three NASDAQ tiers: Global Select, Global Market and Capital Market. The index was developed with a base level of 100 as of February 5, 1971.

Russell 2000 Index: The Russell 100 Index is comprised of the smallest 2,000 companies in the Russell 1000 Index, representing approximately 8% of the Russell 3000 total market capitalization. The real-time value is calculated with a base value of 135.00 as of December 31, 1986. The end-of-day value is calculated with a base value of 100.00 as of December 19,1978.

S&P 500 Index: The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products. The index includes 500 leading companies and captures approximately 80% coverage of the available market capitalization.

MSCI Emerging Markets Index: The MSCI EM (Emerging Markets) Index is a free-float weighted equity index that captures large and mid-cap representation across Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in the each country.

U.S. Aggregate: The Bloomberg USAgg Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (Agency fixed-rate pass-through), ABS and CMBS (agency and non-agency). (Future Ticker: I00001US)

MSCI ACWI Excluding United States Index: The MSCI AC World ex USA Index is a free-float weighted equity index. It was developed with a base value of 100 as of December 31, 1987.

About the Author